Four of the world's largest companies: Amazon, Microsoft, Meta, and Alphabet reported earnings on the same day, within minutes of each other. The collective result was not subtle: 60% earnings growth year-on-year across the group, with revenue growing at roughly 20% at three of the four, and 33% at Meta. For companies of this scale, those are not mature-company numbers. They are the growth rates of businesses a fraction of their size.

And yet the market's reaction split almost immediately. Meta fell 7% in after-hours trading. Alphabet rose 6%. The earnings were similar. The operating income growth was identical at 30% for each. So what was the market actually pricing?

Credibility is the new EPS

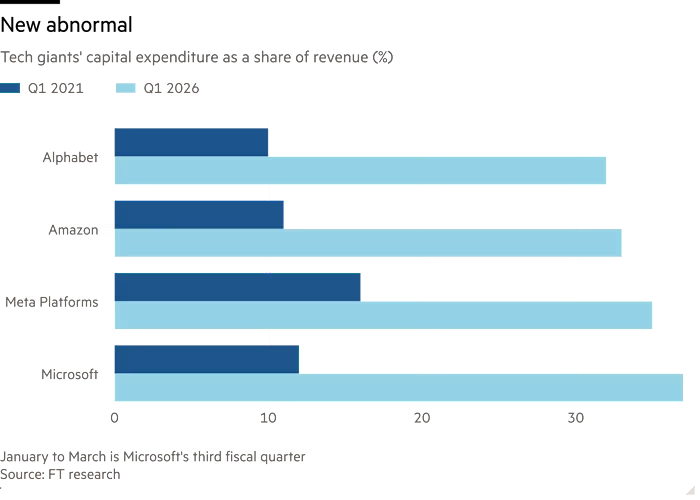

Both Meta and Alphabet announced eye-watering increases to their full-year capex targets. Meta to $145 billion, Alphabet to $190 billion. The divergence in market reaction was not about the size of the spend. It was about whether investors could see what they were buying.

Alphabet has a legible story. Google Cloud is growing. AI-enhanced search queries pushed search-ad revenue up 19% year-on-year. The capex connects to a product that already generates revenue. Investors can build a model around it.

Meta's story is harder to follow. Ad pricing on Facebook and Instagram rose 12%, which is real and valuable. But Muse Spark, its frontier AI model, is not considered competitive at the cutting edge, and the path from $145 billion in AI infrastructure spend to a differentiated AI business is not clearly articulated. The market is not rewarding ambition without a mechanism. It is rewarding ambition with a conversion rate.

Microsoft's AI-related revenue more than doubled year-on-year, reaching roughly 10% of total revenue. Amazon's chip business, powering AI workloads, is growing at a triple-digit rate. These are the numbers that are actually moving long-term valuation assumptions.

The structure of value has shifted

The more consequential story from this earnings cycle is not which company beat by how much. It is what the market is now pricing at all.

Goldman Sachs estimates that three-quarters of the S&P 500's total value now derives from cash flows more than ten years into the future, near the highest level in 25 years. For high-growth tech stocks, that figure is 84%. The practical implication is stark: a 1 percentage point change in assumed long-term growth rates implies a 29% change in enterprise value. Last quarter's revenue beat moves the stock less than a credible signal about who wins the AI war a decade from now.

This is a structural shift in how these companies should be analyzed and held. Short-term earnings volatility matters less. Narrative credibility, who has a convincing answer to the question of where AI revenue actually comes from, matters more than it ever has.

My read

The earnings themselves were not the story this week. The story is that these four companies have collectively more than doubled in market cap since the last time they reported on the same day in October 2020, when their combined value was roughly $5 trillion, and they are still growing like early-stage technology businesses. That is a remarkable fact, and it reflects genuine fundamental progress, not just multiple expansion.

But the valuation architecture built on top of that progress is fragile in a specific way. When 84% of a stock's value lies in terminal-period cash flows, small changes in competitive positioning can have enormous valuation consequences. The sell-off in Meta is a preview of what that looks like: not a bad quarter, just a credibility gap between the size of the bet and the clarity of the payoff. As AI capex continues to scale, every company in this group will face that credibility test repeatedly. The ones that can show the conversion, spend-to-product-to-revenue, will compound. The ones that cannot will look increasingly expensive, regardless of what the quarterly numbers say.