Gold prices have more than doubled since late 2023, repeatedly hitting all-time highs in a sustained rally. The precious metal outperformed major equity benchmarks in 2025 with a 65% return, its strongest single year since 1979, then built on those gains in early 2026.

That kind of performance naturally invites two questions: what is actually driving it, and whether the rally has fundamentally changed what gold is. The answer to both is more nuanced than the headlines suggest.

The traditional drivers, and where they have broken down

Gold has historically been explained by two macro variables: the level of the US dollar and the direction of real yields. Both relationships are real, but neither is operating the way it used to.

On the dollar, the logic is straightforward. Gold is dollar-denominated, so a weaker dollar makes it relatively cheaper for foreign buyers, lifting demand. The DXY is currently around 9% overvalued relative to interest rate differentials, suggesting the dollar environment over the next six to twelve months is likely to be stable to modestly weak, a gentle backdrop for gold. Lingering concerns over Fed independence and US fiscal sustainability are also limiting dollar strength.

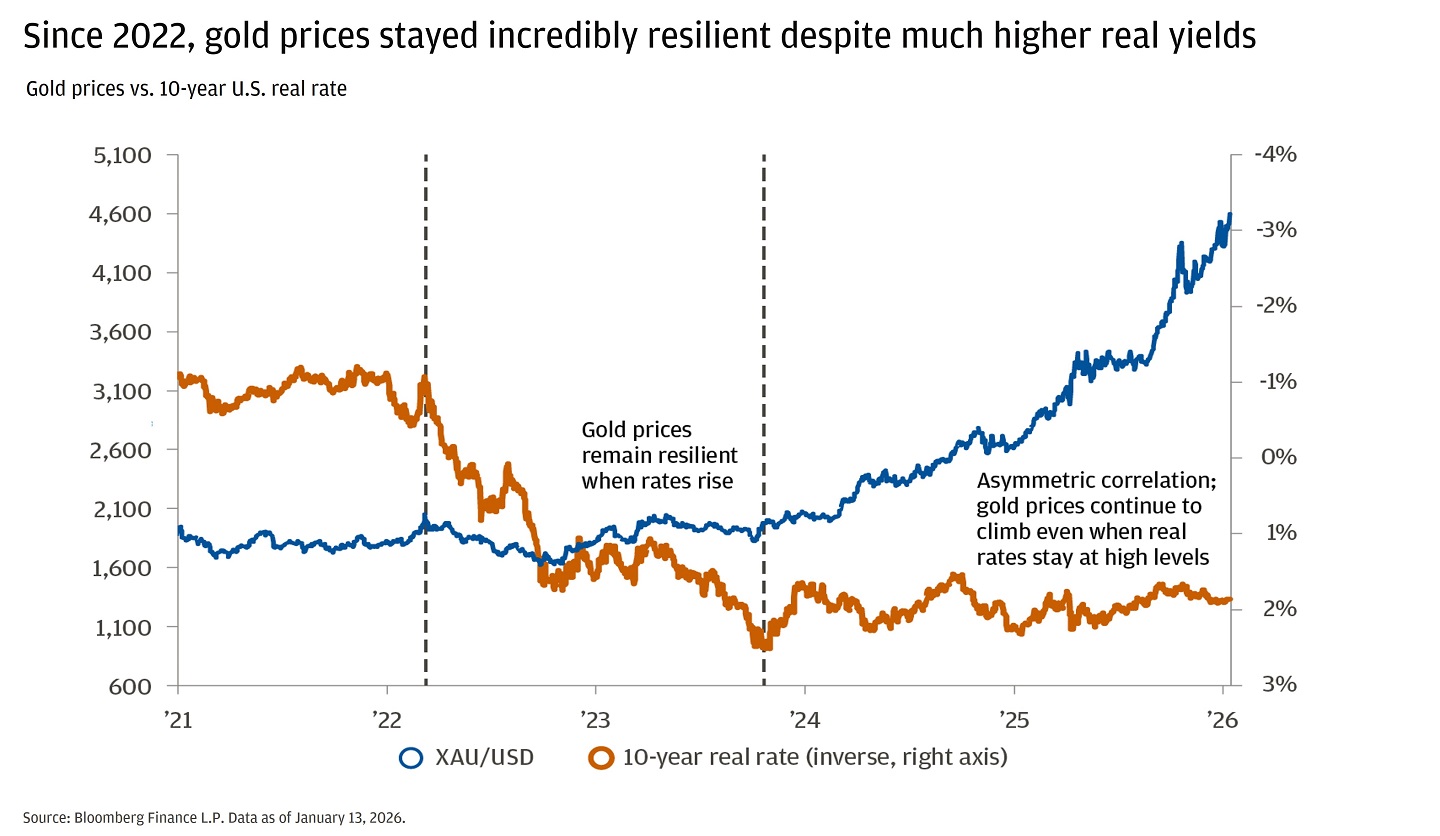

On real yields, a historical inverse relationship holds. Gold rises when real rates fall, because the opportunity cost of holding a non-yielding asset declines, held reliably from the 1990s through 2021. Then in 2022, the Fed raised rates at an unprecedented pace, pushing real yields to their highest levels since the 2008 financial crisis. Yet gold remained resilient: prices were little changed in 2022 and posted a 13% return in 2023, ending that year at a record high.

The correlation has not broken permanently, gold still reacts to real yield movements, but in an asymmetric manner. It rises when yields decrease, but declines to a smaller degree when yields increase. The reason for that asymmetry is a structural shift in the demand picture.

The structural shift: Central banks are buying at scale

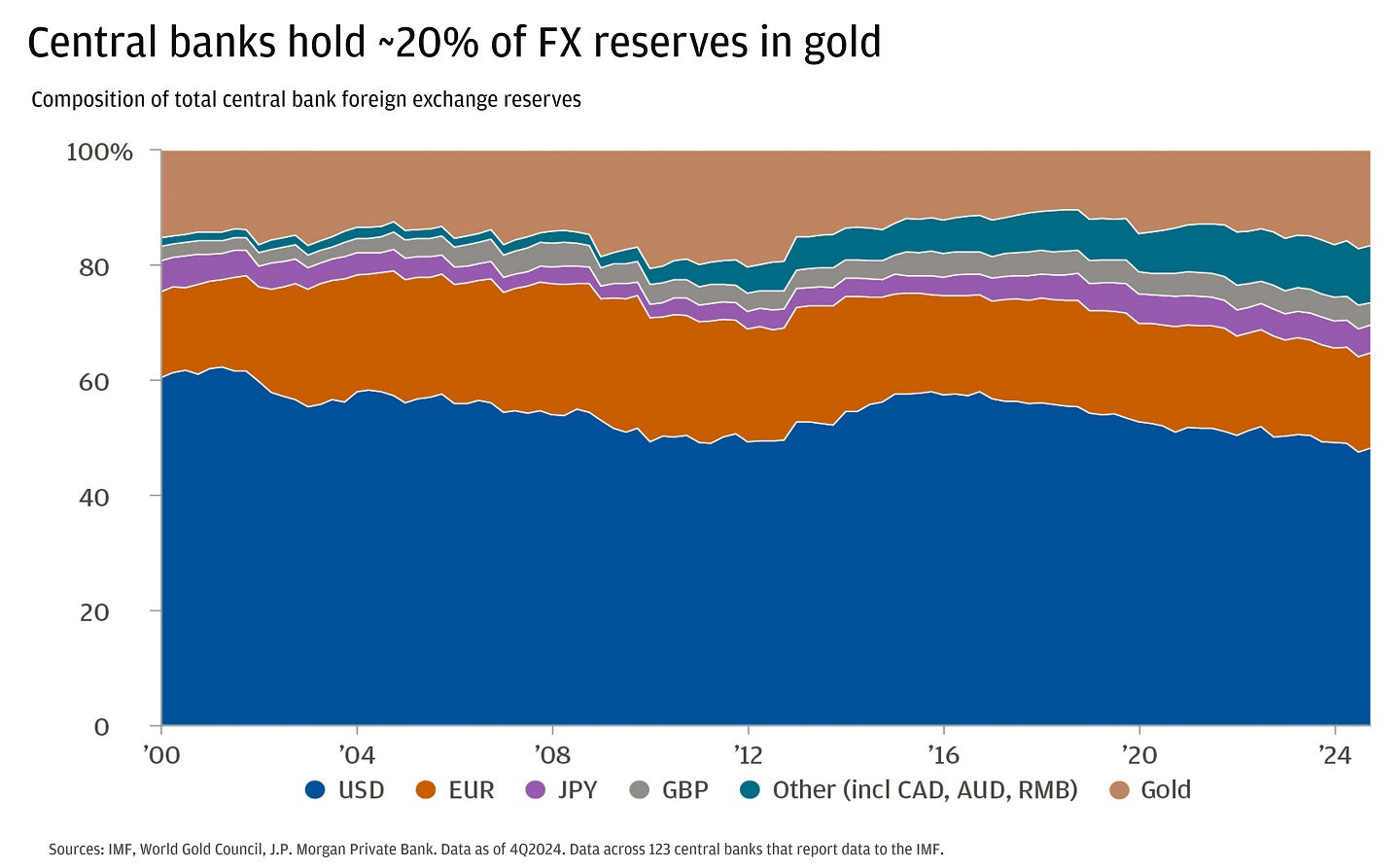

This is the part of the gold story that does not get enough attention in retail investor discussions. The driver of gold's resilience against rising real yields since 2022 is not speculative momentum. It is sustained, large-scale buying by central banks that is providing a persistent demand floor.

Net purchases by central banks reached a record 1,082 tonnes in 2022, more than doubling the average over the previous decade. They sustained that pace in 2023 and 2024, with purchases slowing only slightly in the first three quarters of 2025 despite the sharp price rally. Demand was broad-based and driven by emerging market central banks.

The motivations are structural rather than tactical. Countries facing elevated geopolitical risk are increasing gold reserves. Some nations not allied with the United States are looking to reduce their reserve mix away from dollars to make reserves less vulnerable to sanctions. Other governments are adding protection against a backdrop of higher and more volatile inflation.

The runway for continued buying is significant. China's gold allocation as a percentage of total reserves has risen from 2% in 2000 to 7.7% in 2025. Emerging markets excluding China have moved from 4.2% to 13.2% over the same period. Developed markets sit at 46.5%. The gap suggests EM central banks remain structurally under-allocated relative to peers, and the direction of travel is clear.

A record 43% of 73 global monetary authorities surveyed believe their own gold reserves will increase over the next year.

The retail and institutional layer

Institutional investors tend to hold gold over decades and provide a stable base of demand. The more interesting dynamic in recent years has been retail flows through ETFs, which are more volatile and sentiment-driven.

Gold ETF holdings troughed in early 2024 as elevated cash rates made holding non-yielding gold unattractive. As the Fed began cutting rates and cash yields declined, investors rotated into alternatives including gold. ETF demand picked up in mid-2025 and accelerated rapidly, becoming a primary driver of the sharp 2025 rally. If rates continue to ease, further inflows from retail investors represent a meaningful incremental demand source.

Gold as a portfolio tool, not just a trade

The portfolio case for gold is often framed emotionally, as a hedge against chaos, when the quantitative argument is actually cleaner and more durable.

Over the last five times the S&P 500 declined 20%, gold averaged a 6% return. When US CPI inflation ran between 3% and 4%, gold averaged a one-year return of 13%. Over the past 20 years, gold's annualised volatility has been around 17%, slightly higher than large-cap equities.

That last figure surprises most people. Gold is not a low-volatility asset. Since 1975, it has experienced 91 distinct drawdowns of more than 10%, roughly one every seven months. The S&P 500 has seen 68 such drawdowns. The January 2026 single-day drop of nearly 10% is a reminder that gold can move violently in both directions.

The portfolio argument is not that gold is safe, it is that gold is uncorrelated. Despite its standalone volatility, adding approximately a 5% gold position funded pro rata from a balanced 55/40 stock-bond allocation keeps expected return unchanged while modestly reducing expected volatility. That is a rare combination in portfolio construction.

My read

The bull case for gold is not primarily about geopolitics, even though geopolitics is what gets the headlines. The deeper driver is a structural realignment of central bank reserve management, a multi-year, multi-trillion-dollar reallocation away from dollar-denominated assets that is still in early stages for emerging market institutions. That is not a trade. It is a regime change, and it provides a demand floor that did not exist in prior cycles.

The risk to the bull case is not that the world becomes less uncertain, it is that real yields rise sharply and stay elevated long enough to reverse the ETF inflows that amplified the 2025 rally. Central bank buying would likely cushion that, but it would not prevent a meaningful correction.

JPMorgan's price target of $6,000 to $6,300 per ounce implies meaningful further upside from current levels. Gold is down roughly 2.6% on the week at $4,707 as of this writing, a ceasefire extension and risk-on rotation have trimmed safe-haven demand in the near term. But the structural bid from central banks, the dollar's gradual weakening bias, and the ongoing uncertainty around US fiscal trajectory all point in the same direction over a 12-to-24 month horizon. The recent softness looks more like an entry point than a trend reversal.