The investment case for defence has rarely looked cleaner. Escalating conflicts, fragmenting alliances, and a broad reassessment of national security have pushed governments across the world toward ambitious rearmament plans. Global defence spending is projected to grow at a 5% CAGR through 2030, with earnings expected to grow in double digits after averaging 8% annual growth over the past decade.

But the structural tailwind comes with a constraint that is easy to understate when the headlines are dominated by record budget proposals: most of the countries leading this rearmament cycle are doing so with debt-to-GDP ratios that leave limited room for error.

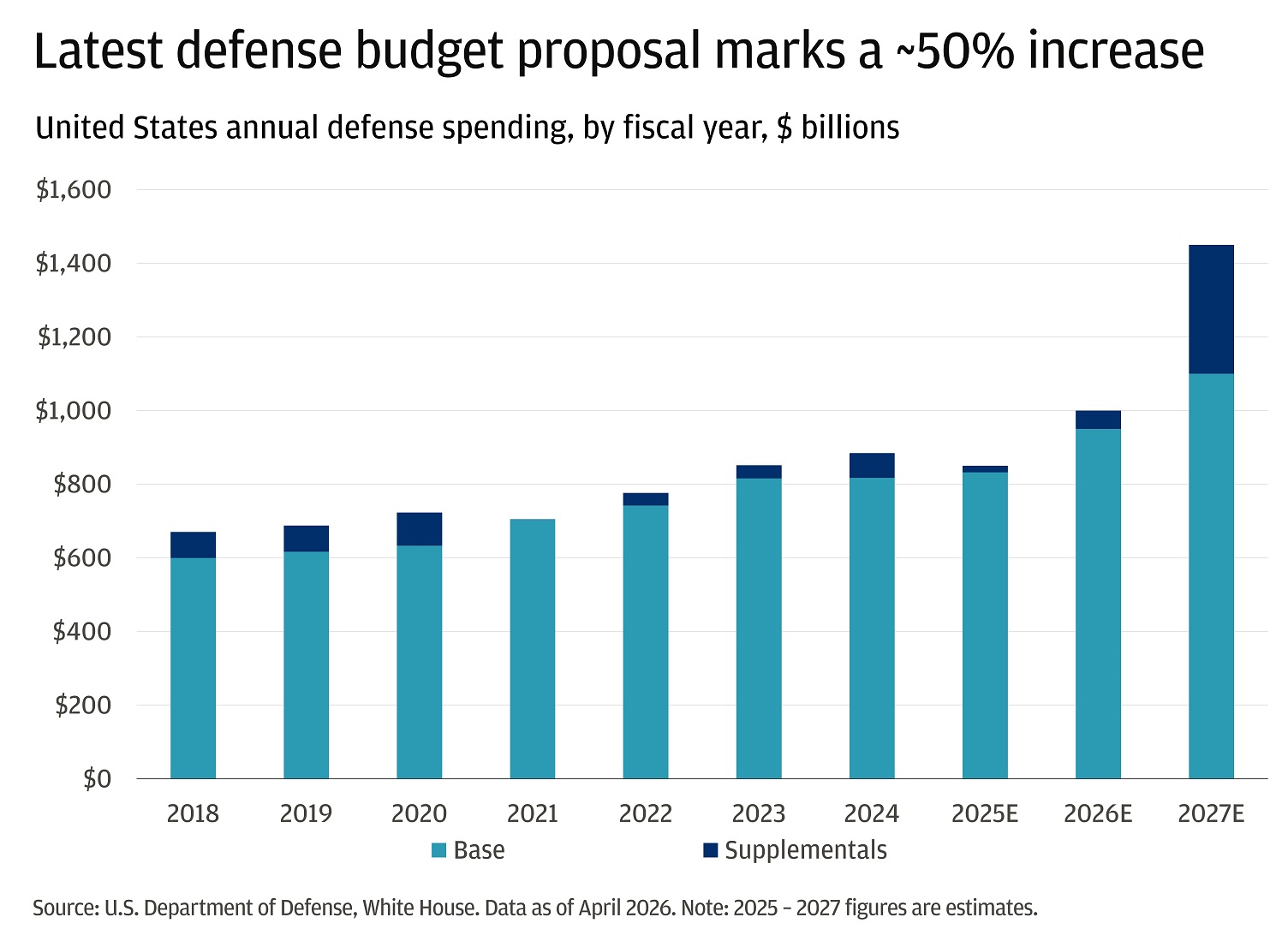

The US: Record ambition, uncertain passage

The United States already allocates approximately a record $1 trillion to defence in fiscal year 2026. A $1.5 trillion budget proposal for 2027 would represent a nearly 50% increase, and that figure does not yet account for supplemental funding requests tied to ongoing Middle East operations.

The composition of the proposal matters as much as the scale. Unlike prior supplemental packages focused on aiding allies like Ukraine and Israel, this proposal leans heavily into domestic priorities, multilayered missile defence systems like the Golden Dome, space capabilities, shipbuilding, AI technology, nuclear funding, and a 5–7% pay raise for troops.

But passage is far from assured. With the US debt-to-GDP ratio above 120% and a global market that has proven increasingly sensitive to fiscal imbalances, even a Republican-majority Congress may push back, particularly in a midterm election year where the scale of spend competes directly with the fiscal priority of reducing the national debt. A scaled-down compromise is the more likely outcome, though even that would represent a meaningful acceleration in procurement and research spending.

Europe: More durable, more constrained

Europe's rearmament story is different in character. Unlike the US, where defence infrastructure is already mature, Europe's challenge is capacity rebuilding from the ground up: munitions, maintenance, logistics, integration. The urgency is crisis-driven, rooted in the war in Ukraine and mounting pressure to meet NATO contribution targets. But uneven industrial readiness across the continent is slowing execution.

Germany is the most striking example of the fiscal trade-off in action. The government boosted military spending by 20–25% in 2025, using both its traditional budget and special Bundeswehr funds, in the process recording its largest public-sector deficit since reunification. Yet even with that investment, Germany's debt-to-GDP sits at just 64%, well below the G7 average of 128%. The fiscal headroom that makes Germany's commitment credible is precisely what most of its peers lack.

The order backlog building across European defence manufacturers tells the story numerically. Rheinmetall's book-to-bill ratio, the measure of new orders accumulating relative to current production capacity, surged to 3.5x in 2025, up from 1.8x in 2024. Orders are arriving nearly three and a half times faster than they can be filled. As an illustrative valuation datapoint, Rheinmetall has been trading at a higher forward P/E than Nvidia for the past 12 months.

Japan: Willing, but constrained

Japan's 2026 defence budget has hit a record 9 trillion yen ($58 billion), a 10% annual increase, driven by political consensus around maritime security and deterrence against China and North Korea. But Japan is attempting this rearmament against a debt-to-GDP ratio of 237%, the highest among developed economies, alongside low purchasing power, ageing demographics, and heavy reliance on foreign energy. The ambition is real. The fiscal constraints are equally real.

My read

The defence sector is one of the more structurally compelling investment themes of this decade, and the valuation case in European names in particular remains interesting given the backlog visibility. But the investment thesis requires a clear-eyed view of what underpins it.

The spending is being driven by genuine geopolitical necessity, that part is durable. What is less certain is the pace of execution. Budget proposals are not budgets, and even when appropriated, translating government spending into revenue for listed defence companies takes time. Supply chains are constrained, manufacturing capacity takes years to build, and the book-to-bill ratios accumulating across European primes reflect real demand that cannot be fulfilled immediately.

The deeper risk worth monitoring is fiscal. The countries with the most urgent rearmament needs are often the ones with the least fiscal room to sustain it. A sovereign debt episode, particularly in a higher-for-longer rate environment, could interrupt spending plans with little warning. Germany is the exception; most others are not.

The opportunity is real, the tailwind is structural, and the backlog visibility is strong. But this is a theme that rewards selectivity over broad exposure, and patience over momentum-chasing. The companies that will compound through this cycle are the ones with the manufacturing capacity to actually deliver, not just the ones catching the headlines.