The Middle East: A Peace Framework, Oil Volatility, and a Long Way to Go

Oil fell below $98 amid hopes of peace talks. It climbed back above $103 by the close. Ceasefire is still in effect.

What Happened

A one-page US-backed peace framework emerged mid-week, reportedly presented to Tehran and awaiting a response within 48 hours. The terms: Iran suspends nuclear enrichment, the US lifts sanctions and releases frozen Iranian funds, and both sides restore transit through the Strait of Hormuz. Brent crude fell as much as 11% on the report before recovering to close down 6.5% on the day at around $103.

Iran's response was characteristically split. The foreign ministry confirmed it was reviewing the proposal through Pakistani mediators. The IRGC-linked Tasnim agency said the proposal contained "unacceptable provisions." Israel conducted its first airstrike on Beirut since April 8 on the same evening.

On Thursday, the situation escalated sharply. The US had struck Iran in response to an attack on American warships exiting the Strait of Hormuz. The ceasefire remains in effect, with Trump simultaneously warning of a far more violent response if provoked further.

Brent swung from near $115 at the start of the week to below $98 on the framework report, back to $103 by close, and then rose again to $102.35 on Friday as the exchange of fire landed. A $17 range inside four trading sessions, with a military engagement bookending it.

Why It Matters

The peace framework and the military exchange define exactly how fragile this situation is. Diplomacy and live fire are happening simultaneously.

Markets responded immediately to the framework. European equities surged, with the Stoxx 600 and FTSE 100 both gaining 2.2%. Asian markets followed. The Nikkei 225 soared 6% on Thursday, South Korea gained 1.1%, Taiwan 2.2%. Japan, in particular, is the most direct beneficiary of any Hormuz resolution, given its 90% dependence on Middle Eastern crude imports. The scale of those moves reflects just how much geopolitical risk premium is embedded in non-US assets and how quickly it could reprice in either direction.

The oil market is threading a needle. The partial de-escalation implied by peace talk headlines is real enough to compress the risk premium. The exchange of fire is real enough to keep it from collapsing entirely. Brent in the low $100s is the market's best current estimate for a situation where resolution is possible but not imminent, and where the next headline, in either direction, has an outsized price impact.

Samsung Hits $1 Trillion: The Memory Trade Is No Longer Being Ignored

14% in a single session. The Kospi is above 7,000 for the first time. And a valuation that is still, by any measure, cheap.

What Happened

Samsung Electronics surged more than 14% on Wednesday to hit a $1 trillion market capitalization, becoming only the second East Asian company to join that club alongside TSMC. SK Hynix leaped more than 10% on the same day. The catalyst was AMD's after-hours forecast beat, which signaled to the market that AI chip demand was not softening. Samsung's Q1 operating profit came in at 57.2 trillion won ($39 billion), more than eight times the same period last year. The Kospi crossed 7,000 points for the first time, capping a 70% year-to-date gain.

Why It Matters

Samsung's re-rating reflects something structural, not just momentum. HBM chips, the high-bandwidth memory that Nvidia's GPUs depend on, are now a strategic bottleneck in the AI supply chain. Hyperscalers are locking in multi-year supply contracts. Prices for less advanced DRAM and NAND have also been pulled higher by the demand overflow. The business has structurally transformed from a cyclical commodity producer into critical AI infrastructure.

The valuation gap remains striking. Samsung trades at roughly 6x forward earnings. TSMC trades at 25x. Micron at 10x. That discount reflects residual skepticism about memory cyclicality, but analysts are right to note that the discount looks increasingly difficult to justify as earnings visibility improves through long-term contracts. The near-term risk worth monitoring: Samsung unions have flagged a strike from May 18 if a bonus deal is not reached, and the internal tension between the semiconductor division's windfall and other divisions' exclusion from it is a genuine operational risk.

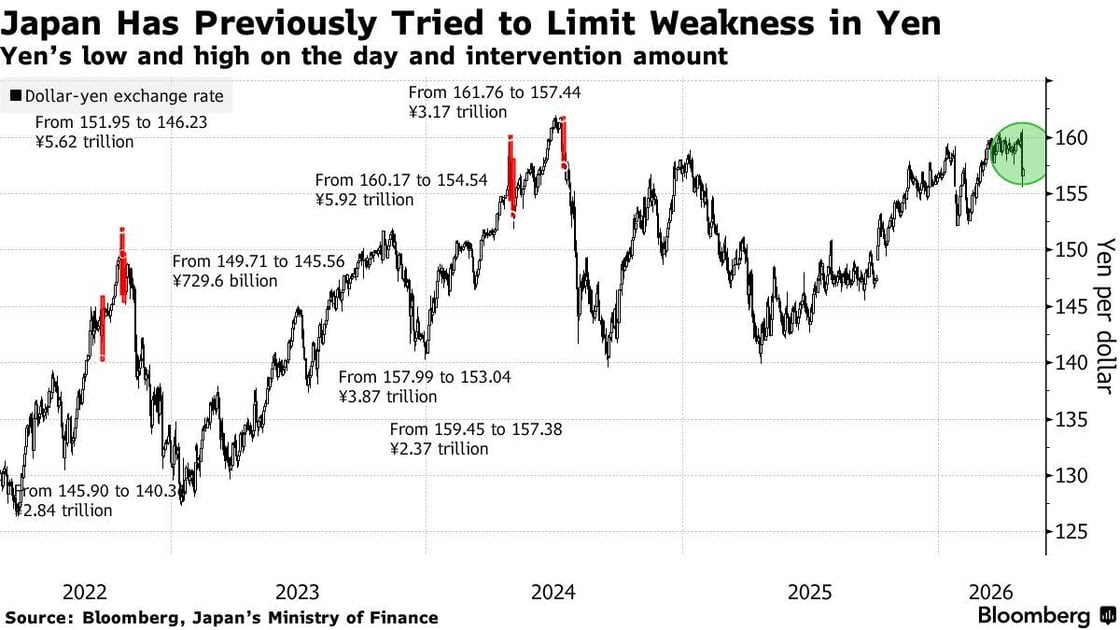

Japan's Yen: The Second Intervention in a Week. And Why Neither Is Sticking

Yen surged from 158 to 155 in thirty minutes. By the next session, it was drifting back.

Japan conducted its second suspected currency intervention of the week on May 6, following a confirmed intervention the prior week. The pattern is becoming familiar: the yen weakens toward the 158 to 160 level, authorities step in, the yen surges, and then the carry trade reasserts itself, and the gains erode within sessions.

The structural problem is not new, but it is getting worse. The BOJ's 0.75% policy rate remains far below those of other major central banks. The US-Japan rate differential, historically defined by Japan's ultra-low rates, now has a second driver: Trump-era inflation fears and policy uncertainty are pushing US yields higher, keeping the differential wide from both ends. Japan has added its own inflation risk premium through Prime Minister Takaichi's fiscal expansion and preference for accommodative monetary policy.

The resumption of a longer-term appreciating yen trend appears unlikely, particularly as overseas central banks are striking a hawkish tone. USD/JPY is expected to remain elevated in the medium term - Barclays

The intervention provides short-term relief and sends a political signal domestically. Takaichi won her election on a promise to protect households from rising prices, and a ¥160 yen contradicts that directly. But without either a meaningful BOJ rate increase or a sustained narrowing of the rate differential, these interventions are buying weeks, not trend reversals. The June BOJ meeting, where a hike is increasingly being telegraphed, is the more consequential catalyst to watch.

A Resilient U.S. Labour Market

115,000 jobs added in April, beating expectations for the second month running. The labour market is holding for now.

April payrolls came in at 115,000, well ahead of the 65,000 economists had forecast. The unemployment rate held at 4.3%. Healthcare, retail, and transportation drove the gains, while federal government employment continued to slide and the tech sector shed jobs. Jobless claims remain historically low at 200,000, with continuing claims falling to a two-year low of 1.77 million.

Several cautionary considerations for the market. February's reading was revised further downward to a net loss of 156,000, a reminder of how volatile the monthly data has become and how difficult it is to read a clean trend from any single print.

On the same day, the University of Michigan's consumer sentiment index fell to a fresh record low in May, driven by inflation fears from the energy shock. Companies are still hiring. The people being hired are increasingly pessimistic about their financial situation.

Why It Matters

The April report keeps the Fed's calculus firmly on hold. A labour market adding jobs above expectations, with unemployment steady at 4.3%, gives the Fed no justification to cut against a backdrop of 3.5% headline inflation.

The more important signal is the divergence building underneath the surface. The labour market is a lagging indicator. Consumer sentiment is already deteriorating. If spending softens further under the weight of $4 gas, hiring will follow, and by the time that shows up in payroll data, the demand-side weakness will already be well underway. Cleveland Fed president Beth Hammack said it plainly: "If you see that demand side coming under pressure, that could be in jeopardy on the employment side of our mandate."

Markets took the report positively. The S&P 500 gained 0.8% to close at a record high. For now, a resilient labour market combined with AI earnings momentum gives equities a runway. The risk is that resilience will not last as long as the market is currently pricing in.

View Forward:

An important dynamic in markets right now is the widening split between accelerating AI-driven investment spending and a US consumer that is quietly deteriorating. Q1 GDP looked fine at the headline, but the composition did not. Consumer spending at 1.6% annualized, savings rates falling, and gas above $4 not yet fully reflected in the data. Q2 will show it more clearly. The market is priced as though only the investment side of that equation exists.

The wildcard that changes everything is Hormuz. A deal that reopens the strait and brings oil back toward $80 to $85 immediately relieves consumer pressure, reopens the rate cut path, and compresses the valuation gap between AI infrastructure plays and consumer names that the current consensus depends on. That scenario is not priced, and this week's US-China summit makes it more relevant.

Trump heads to China this week for his first official visit since 2017, in what is the most consequential diplomatic meeting in years. Trade and tariffs will dominate the agenda, but the Hormuz question sits underneath it all. Washington has been pressing Beijing to use its influence with Iran to reopen the strait, an outcome that serves both economies. China's rare earth dominance remains its most powerful bargaining chip, and the AI race adds another layer of tension, with the US holding a narrowing technology lead against Chinese infrastructure buildout. Few expect major breakthroughs. But with US midterms on the horizon, Trump will be looking for wins, and this president has a history of surprising.

On Japan, the yen interventions are not sticking structurally and will not until the rate differential narrows from both ends. The June BOJ meeting is the real test; a hike combined with any softening in US yields could trigger carry trade unwinding faster than most positioning can absorb. Unhedged Japan exposure carries more asymmetric risk than it appears.

On semiconductors, the supercycle thesis is intact, but the easy re-rating is done. SOX up 40% from the March trough means returns from here are driven by earnings delivery, not sentiment.

Weekly Market Snapshot

Indices

SPX: +2.33%

NDX: +5.50%

SOX: +11.14%

VIX: +1.18%

Treasuries

US 2Y: +0.13%

US 10Y: -0.54%

FX

USD/JPY: -0.24%

USD/CNH: -0.51%

Commodities

Brent: -7.66%

XAU/USD: +2.16%

On the Radar

Date | |

|---|---|

Monday 11/05 |

|

Tuesday 12/05 |

|

Wednesday 13/05 |

|

Thursday 14/05 |

|

Friday 15/05 |

|