There is a moment in every capital cycle when the numbers stop looking like investment and start looking like obligation. For Big Tech, that moment is now.

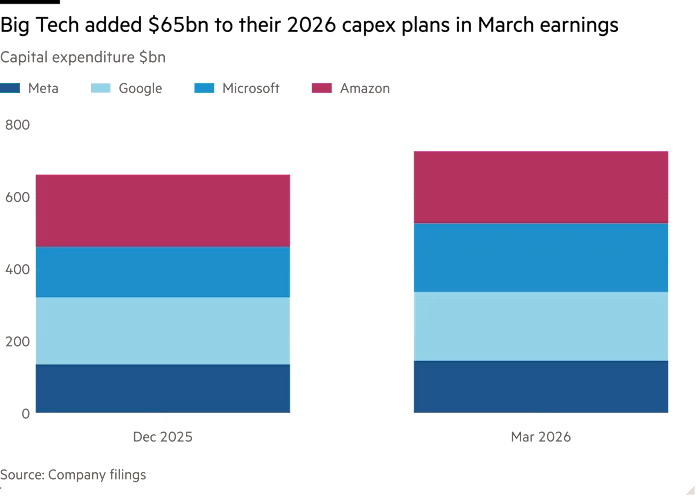

Amazon, Alphabet, Microsoft, and Meta are collectively spending $725 billion on AI infrastructure this year, a 77% increase from last year's record. The result is a free cash flow picture that has not looked this strained since 2014, when these companies were generating roughly a seventh of their current revenue. Combined quarterly free cash flow is expected to fall to approximately $4 billion in Q3, compared with an average of $45 billion per quarter since the pandemic. Amazon is expected to burn net cash for the full year. Meta will burn cash in the second half. Microsoft in at least one quarter. Alphabet's full-year free cash flow will be its lowest in over a decade.

These are not small companies running on thin margins. These are the most profitable businesses in the history of capitalism, and they are spending faster than they earn.

From cash machines to infrastructure companies

The transformation is structural and it happened quickly. Five years ago, Big Tech's defining financial characteristic was its asset-lightness: software margins, minimal capex, enormous free cash flow returned to shareholders through buybacks and dividends. That model is being deliberately dismantled in real time.

Alphabet bought back no stock in Q1 for the first time since its repurchase program began in 2015. It has issued $48 billion in new debt in the past two months alone. Meta has issued $55 billion in debt over six months while pausing buybacks for the longest stretch since it began repurchasing shares in 2017. Microsoft's balance sheet assets in servers, networking equipment, and software have more than tripled since mid-2022, from $61 billion to $191 billion.

The companies that once defined capital efficiency are now running capital cycles more familiar to telecoms operators or chemical manufacturers than to software businesses.

"The real free cash flows of many hyperscalers are probably worse than what they call their free cash flows." - Christian Leuz, University of Chicago Booth School of Business

That last point deserves more attention than it is getting. "Free cash flow" is not a standardized accounting metric. Companies have discretion in how they treat share-based compensation, leased data centers, and off-balance-sheet structures. Meta, alongside others, has shifted tens of billions in data center projects into special-purpose holding vehicles that attract outside capital and raise debt that does not fully appear on the corporate balance sheet. Oracle, pursuing a $300 billion data center contract with OpenAI, began burning cash last year and is not expected to return to positive free cash flow until 2030. The reported numbers are the optimistic version of the story.

The prisoner's dilemma framing is the right one

Amazon's Andy Jassy reached for the AWS analogy to explain the capital commitment, a bet that weighed on the balance sheet for years before becoming the source of more than half the company's profits. It is a reasonable parallel, and the logic is sound: AI infrastructure built today will generate returns over a decade-long horizon, and early-year free cash flow compression is the price of getting there first.

But the AWS analogy has a limit. AWS was a genuinely new category that Amazon was building largely on its own. The current AI infrastructure race is being run by four companies simultaneously, each spending at a scale that assumes they will capture a disproportionate share of the returns. They cannot all be right. The prisoner's dilemma framing, each company compelled to invest because its competitors are investing, regardless of whether the aggregate return justifies the aggregate spend, is not a pessimistic interpretation of what is happening. It is an accurate one.

The University of Chicago's Leuz put it plainly: this resembles the capital cycles seen in telecoms and chemicals, where over-investment eventually leads to overcapacity, depressed margins, and weak returns. Tech CEOs know this. They are investing anyway, because the alternative, falling behind on a technology they genuinely believe will be transformational, is worse than the risk of overcapacity.

What the free cash flow compression is actually telling us

I think the market is right to look through near-term free cash flow weakness, up to a point. These companies entered this cycle with fortress balance sheets, the debt being issued is cheap relative to the return profile of the assets being built, and the earnings trajectory, cloud growth, AI monetization, and ad pricing are validating the thesis in real time. A temporary period of negative free cash flow in businesses generating $200 billion in annual revenue is not the same as financial distress.

But there are two things worth watching that are not fully reflected in the current consensus.

The first is cost inflation within the buildout itself. Microsoft flagged $25 billion in additional capex this year, attributable purely to component cost inflation, memory chips, networking equipment, and power infrastructure. Meta cited the same pressure. This is not a one-off. If memory prices continue rising as the supercycle thesis suggests, and if GPU availability remains constrained, the cost side of this equation keeps moving against the hyperscalers even as they scale revenue. Margin compression from the supply side is a different and less visible risk than the demand-side questions the market is debating.

The second is what happens to shareholder return expectations when the cycle turns. These companies have spent years conditioning institutional investors to expect aggressive buybacks and growing dividends. Alphabet is pausing repurchases entirely, and Meta is doing the same. These are not small signals. When free cash flow recovers and buybacks resume, the market will cheer. But there is a window of several quarters, perhaps longer, where the capital return story is effectively suspended. For investors who own these names partly on a capital-return basis, that repricing has not fully materialized yet.

My read

The investment thesis for Big Tech is not broken by the free cash flow compression. But it has changed shape. You are no longer buying capital-light compounders that return cash reliably while growing revenue. You are buying companies running a decade-long infrastructure bet, funded partly by debt and off-balance-sheet structures, in a capital cycle that none of them can exit unilaterally.

The bull case requires believing that AI monetization scales fast enough, and that the market structure that emerges favors the incumbents over the challengers. The first condition is showing early signs of being met; cloud growth is real, and AI revenue is converting. The second is less certain. Anthropic approaching a $1 trillion valuation, OpenAI at $852 billion, and SpaceX assembling its own AI stack are not the competitive dynamics of a market being locked up by the hyperscalers. The infrastructure is being built. Who captures the value at the application layer remains genuinely open.

That is the question this $725 billion is ultimately trying to answer. The market is pricing it as though the answer is already known.