There is a version of the current market that looks like a collective delusion. A two-month war in the Middle East, Brent above $100, a Fed that cannot cut, a consumer that is quietly slowing, and US equities sitting at all-time highs. The instinct is to call it irrational exuberance, to reach for historical analogies about markets climbing walls of worry until they suddenly don't.

I think that instinct is wrong. But I also think the people acting on the bullish case are underestimating how narrow the foundation beneath them actually is.

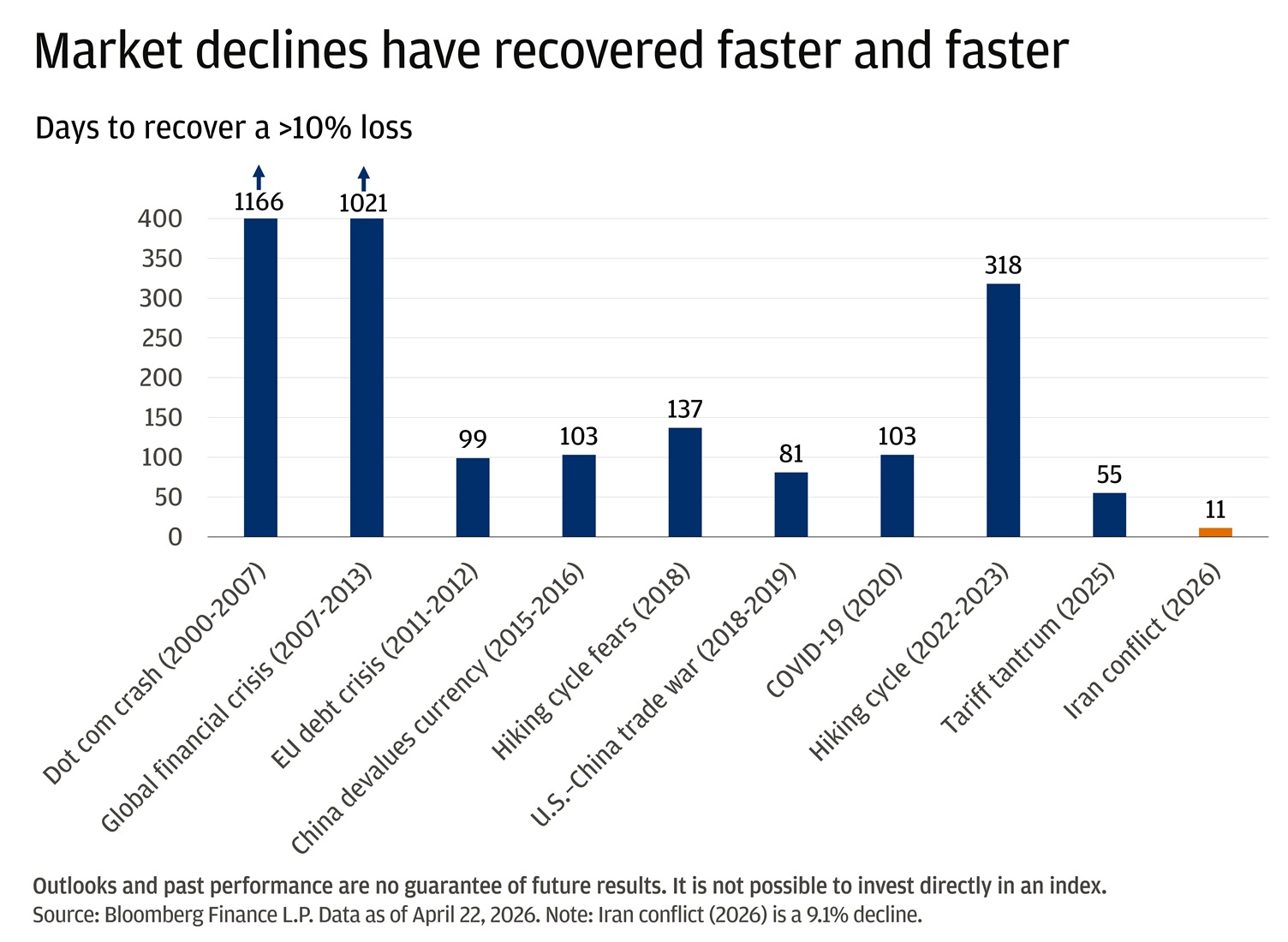

Recoveries have been structurally compressing for years

The speed of the rebound from the February sell-off was striking but not unprecedented in recent history. What was once measured in years now takes weeks. The dot-com recovery took over 1,000 days. The GFC took roughly the same. COVID took just over 100. The tariff shock of 2025 took 55. This recovery happened in days.

The reason is not that investors have become reckless. It is that markets have become structurally better at absorbing geopolitical shocks. Liquidity is deeper. Risk management is more sophisticated. And perhaps most importantly, institutional memory has been trained by a decade of shocks that ultimately resolved without permanently impairing long-term earnings power. Investors who sold during COVID, the 2022 rate shock, or the 2025 tariff escalation were wrong to do so. The market knows this. It acts accordingly.

That behavioural shift is rational given the evidence. It is also precisely what makes the next genuine structural break so dangerous when it arrives, because the trained response will be to buy the dip one more time.

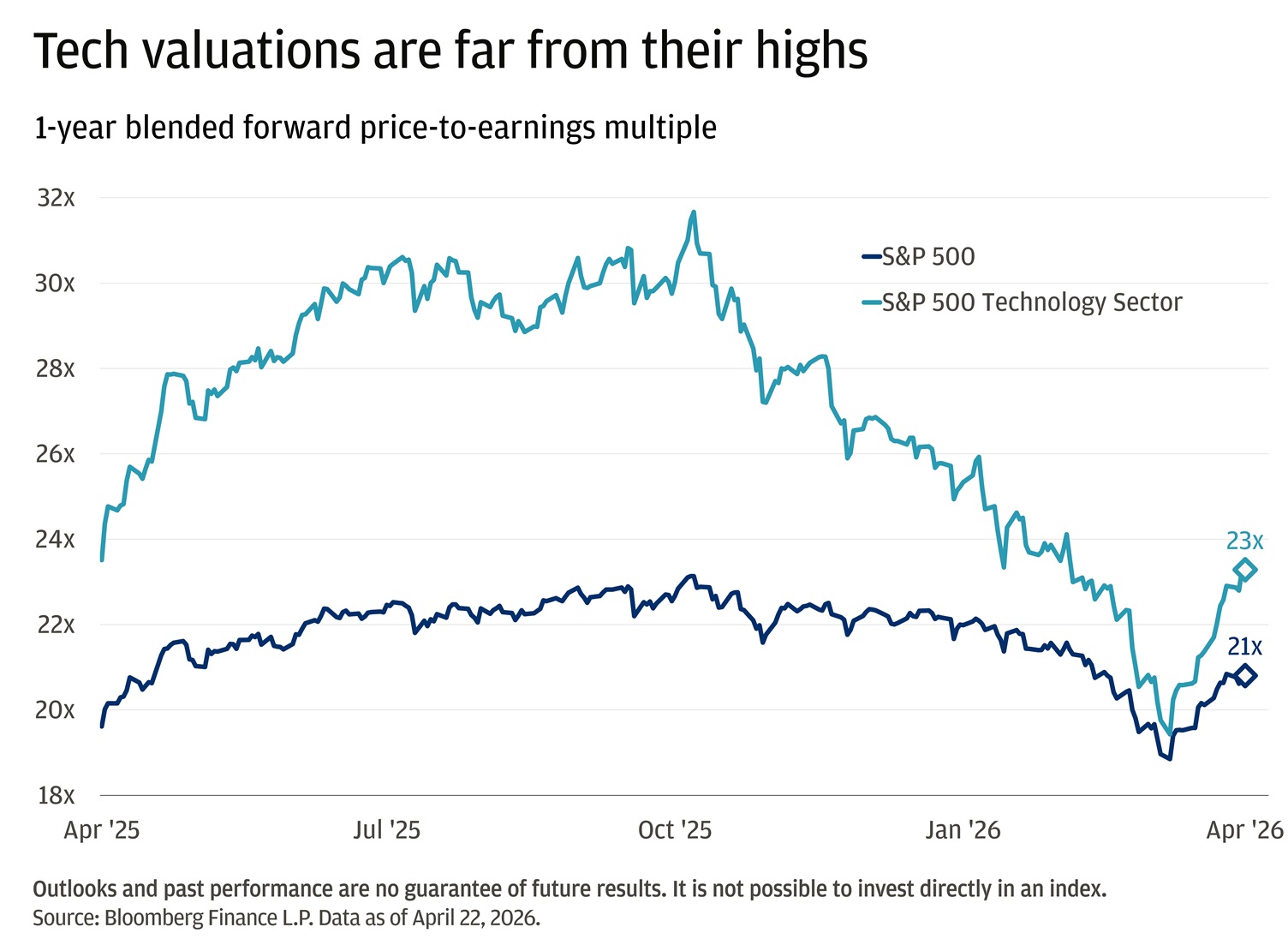

The price is back. The valuation is not.

Here is the part of this recovery that deserves more attention than it gets. The S&P 500 is back at its highs, but it is not back at its peak valuation. At the end of 2025, the index traded above 23x one-year blended forward earnings. Today it sits below 21x. In technology, the compression is more pronounced.

What that means is that the price recovery has been funded by earnings expectations rising faster than prices, not by multiple expansion. The market is re-rating on fundamentals, not sentiment alone. That is a more durable signal, and it is one reason the bulls have a defensible case that this is not simply a euphoric overshoot.

The outcome is equally important. If earnings expectations are now doing the work, then a disappointment in earnings, not a geopolitical escalation, is the more credible threat to the rally. The war is known and partially priced. A quarter where hyperscaler capex guidance rises faster than revenue does not yet have a price attached to it.

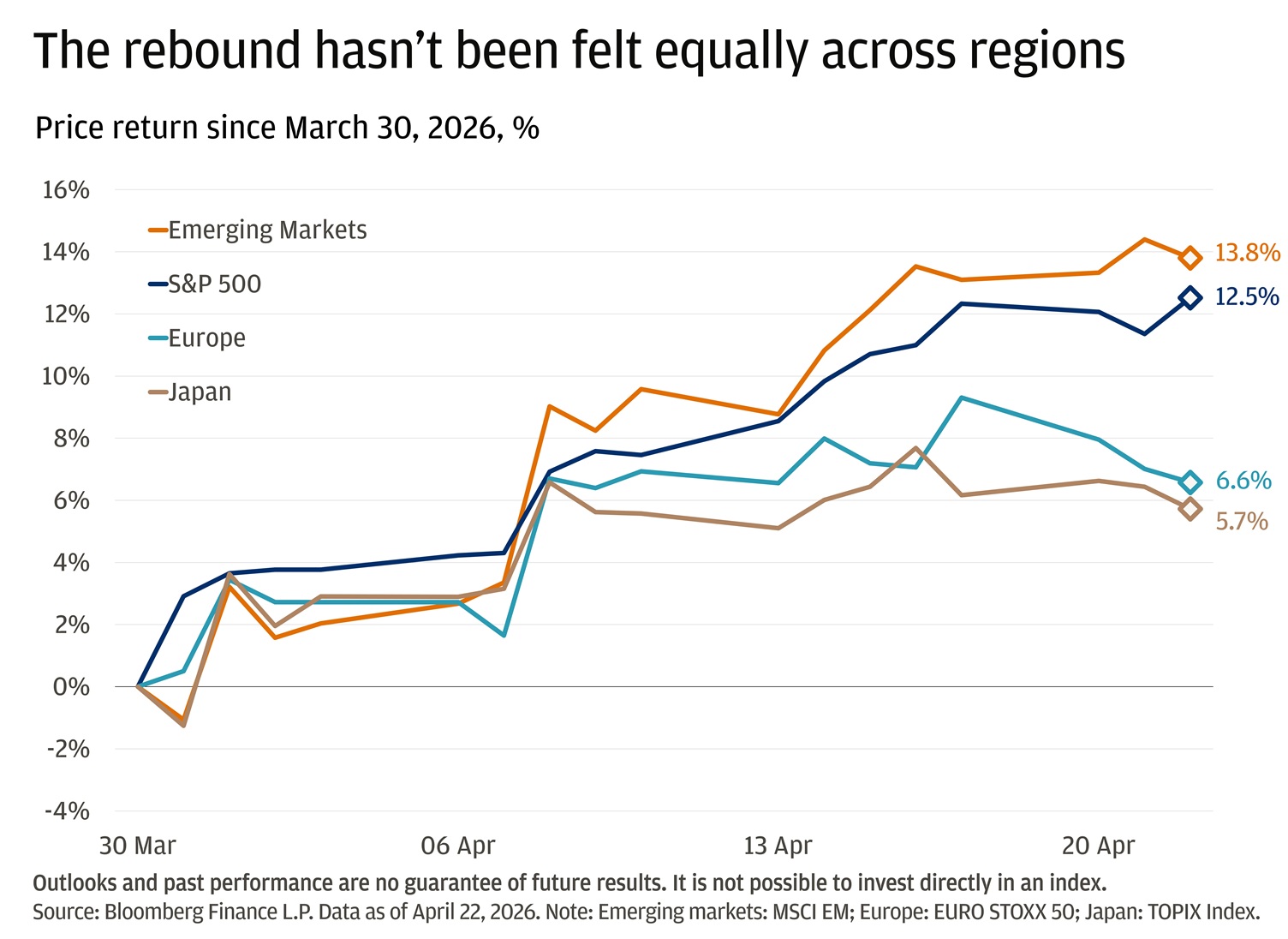

The geographic divergence is telling you something real

US equities are at records. Europe and Japan, despite fierce rebounds, remain below their pre-conflict peaks. That gap is not noise, it is structure.

Europe entered this crisis with elevated valuations, aggressive earnings expectations, and an economy far more directly exposed to energy price shocks than the US. It has no meaningful technology weighting to absorb the AI re-rating that has insulated US indices. The result is negative earnings revision risk that does not exist in the same way on the US side of the Atlantic.

Asia's divergence is of a different character. Korea and Taiwan have roared back, both are direct beneficiaries of AI chip demand that is indifferent to Hormuz. Japan has partially recovered but remains constrained by yen weakness and energy import dependence, which no domestic earnings cycle can fully offset.

The lesson is not that US exceptionalism is permanent. It is that in this specific crisis, the US happens to sit at the intersection of the two structural forces that matter most: a net energy exporter and home of the AI capex cycle, and that combination is genuinely difficult for other markets to replicate. When those two advantages fade or reverse, the divergence closes. Until then, the gap is earned, not irrational.

What the rally is actually betting on

Strip away the noise and the market is making one large, concentrated bet: that AI-driven earnings growth is durable enough, and broad enough across the hyperscaler ecosystem, to justify current valuations through the energy shock and the consumer slowdown simultaneously.

The evidence so far supports that bet. Earnings have beaten expectations at an above-average rate. Revenue growth is on track for its strongest reading since 2022. Six consecutive quarters of double-digit earnings growth would be the longest such streak since the post-GFC recovery. Cloud growth is real and accelerating. AI revenue is converting, not uniformly, but at scale in the names that matter most for index returns.

But the bet has a specific vulnerability that is not fully appreciated. Goldman Sachs estimates that roughly three-quarters of S&P 500 value now derives from cash flows more than ten years into the future. For high-growth tech stocks, that figure is higher still. The practical implication: a 1 percentage point change in long-term growth assumptions moves enterprise value by nearly 30%. The market is exquisitely sensitive to anything that shifts the perceived durability of the AI earnings trajectory, far more sensitive than a headline P/E ratio suggests.

My read: justified but fragile

The record highs are not irrational. They reflect a genuine earnings acceleration, a structural insulation from energy shocks, and a capital gravity that pulls global institutional flows toward the only major market with both yield and growth. I would not fight the tape on that basis alone.

What I would do is be precise about the risk being taken. The rally is narrow. It is concentrated in a handful of names whose valuations are now doing the work of pricing a very specific long-term future. The geopolitical risks have been absorbed, but only by assuming they resolve, not by assuming they don't matter. A Hormuz deal that fails, a quarter of AI capex that overshoots revenue, or a consumer deterioration that bleeds into corporate spending would each force a rapid reassessment.

The wall of worry has been climbed efficiently and repeatedly. That is both the bull case and, in a market priced this precisely for a particular future, the source of its greatest fragility. Records are made to be tested. The question is not whether this one will be, it is what does the testing.