The Rally: Nine Weeks and Counting

S&P 500 up 16% since the end of March. Nasdaq up 25%. The Philadelphia Semiconductor Index is up 81% this year, on track for its best annual return since the dotcom bubble.

The S&P 500 closed its ninth consecutive week of gains, its longest winning streak since December 2023, rising 1.4% on the week and hitting record closing highs on 11 of May's 22 trading days. The Nasdaq has soared almost 25% since the end of March. The Philadelphia Semiconductor Index is up 81% this year and is on track for its largest annual return since the dotcom bubble.

The numbers at the individual stock level are harder to contextualise. SK Hynix, Micron, and Samsung are up 1,000%, 900%, and 470% respectively over the past 12 months. Intel and AMD are up 490% and 350%. These are not incremental re-ratings. They are complete valuation reconstructions.

The week's standout was Dell. Revenue rose 88% to $43.8 billion in its fiscal Q1, with AI server sales, powered by Nvidia chips, jumping 757% to $16.1 billion year-on-year. Full-year revenue guidance of up to $169 billion blew past the $142 billion analyst consensus. Dell shares surged 33% in a single session, building on a 225% increase in share price from February, after a $9.7 billion Pentagon contract win. A server company, a business that most investors had filed under "legacy hardware", is now one of the most discussed stocks on Wall Street.

"We're in full-on mania. The growth multiples the market is putting on AI companies are insane. They assume we're going to see this sort of revenue growth for years and years to come." - Mike O'Rourke, Jones Trading

The Ceasefire: A Deal That Is Close But Not Done

Brent fell 11% on the week to $92. Trump says he is close to a "final determination." Iran says talks are ongoing.

The Framework

After weeks of fragile back-and-forth, the broad outlines of a ceasefire extension agreement are now visible. Under the proposed memorandum of understanding, Iran would gradually allow the Strait of Hormuz to reopen and remove mines from the waterway over the first 30 days. Negotiations on Iran's nuclear programme would run in parallel, with Tehran agreeing to discuss diluting or handing over its stockpile of highly enriched uranium and committing not to develop a nuclear weapon. The US would, in phases, provide sanctions relief and unblock Iranian assets held overseas, conditional on progress toward a final pact, while easing its naval counter-blockade on Iranian ports.

Trump laid out his public terms on Friday: no nuclear weapons, Hormuz open immediately with no tolls, and mines to be removed. Notably, he said no money would be exchanged until further notice, walking back the sanctions relief component that had been central to prior Iranian asks.

Where It Stands

Both sides have signalled proximity to a deal while flagging unresolved issues. The gap between a 30-day enrichment suspension, which Iran has shown initial openness to, and Trump's demand for a 20-year moratorium without a sunset clause remains the core sticking point.

Oil has priced in significant progress. Brent settled at $92.05 on Friday, a six-week low, down 11% on the week. If a deal is signed, $80 to $85 is plausible within weeks. If it falls apart, the reversal will be sharp.

SpaceX: The Biggest IPO in History Is Two Weeks Away and Markets May Feel It

$86.5 billion raise. A $2 trillion valuation. And a listing that will mechanically extract more cash from equity markets than any event in history.

SpaceX begins trading on the Nasdaq on June 12. The company will raise approximately $86.5 billion, more than five times Facebook's 2012 IPO and nearly four times Alibaba's 2014 listing. At a market cap of up to $2 trillion, it would enter the S&P 500 and Nasdaq immediately as one of the most valuable companies in both indices.

The scale of the capital requirement is the story. Passive funds tracking the S&P 500 are expected to take down roughly $44 billion to reflect SpaceX's weight in the index, with Nasdaq and Russell 1000 trackers adding further demand. Active managers benchmarked against those indices bring the total institutional absorption requirement to nearly half the float. That is not routine IPO demand. It is a structural reallocation event.

The concern that is starting to surface among serious market watchers is arithmetic, not sentiment. Cash directed into SpaceX comes from somewhere. With hyperscaler buybacks already pared back to fund AI capex, one of the market's traditional demand pillars is absent precisely when new supply is at its largest. A reduced lockup period means early SpaceX investors can begin exiting as soon as the end of Q2.

"There is no historical precedent to such a capital raise. I think it will place a huge test on the stability of the US equity market." - Rupert Mitchell, Blind Squirrel Macro

View Forward

The bull case for this market is not hard to state. First-quarter earnings beat broadly. Goldman Sachs and Morgan Stanley have both raised their S&P year-end targets in recent weeks. AI investment spending is translating into real revenue. Dell's numbers this week are the most recent proof. The Fed is on hold rather than hiking. And a Hormuz deal, if it arrives, removes the single largest macro headwind in one move. Goldman's Ben Snider put it plainly: the conditions that typically end bull markets, speculative mania translating into contracting margins, or a Fed actively tightening, are absent.

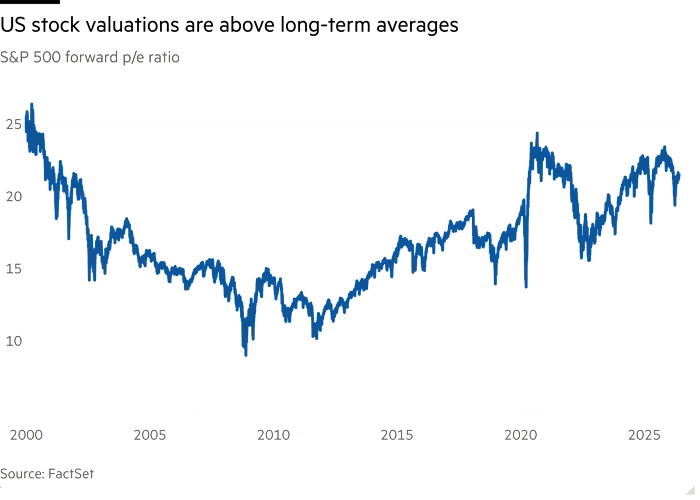

The S&P 500 is trading at 21 times forward earnings against a 30-year average of 17. That premium can be justified by structurally higher earnings growth, and if the AI cycle delivers what the current capex wave implies. A reminder that valuation compression, when it comes, does not require a fundamental deterioration. It only requires the pace of positive surprise to slow.

The dynamic to watch most carefully is not whether AI earnings keep beating, they probably will for another few quarters. It is whether the multiple the market is willing to pay for those earnings begins to compress as the Hormuz situation resolves and the macro environment normalizes. When the geopolitical risk premium derived from oil declines, the safe-haven narrative for US tech weakens. When the Fed eventually has room to cut, the relative attractiveness of long-duration growth assets softens at the margin. The same resolution that would feel like a relief rally in the short term contains the seeds of a valuation re-rating in the medium term.

None of this argues for selling. Morgan Stanley's Mike Wilson said it directly: pockets of excess and 15-20% corrections in individual names are possible, but the market can keep marching forward. Earnings durability is a key anchor. If the AI-driven earnings cycle is multi-year and not front-loaded, then current multiples are defensible on a through-cycle basis.

The risk is not collapse. It is the gap between what the market is pricing and what the next twelve months can realistically deliver. At 21x forward earnings, after nine straight weeks of gains, and an 81% semiconductor index move in five months, the market is not wrong, but it is priced for everything to go right. A ceasefire deal, a soft landing, AI monetisation on schedule, and no Fed surprises. That is a narrow path. Wide enough to keep walking, but not so wide that you can afford to stop watching your footing.

Weekly Market Snapshot

Indices

SPX: +1.43%

NDX: +2.89%

SOX: +5.14%

VIX: -2.67%

Treasuries

US 2Y: -0.61%

US 10Y: -0.18%

FX

USD/JPY: +0.01%

USD/CNH: -0.13%

Commodities

Brent: -11.59%

XAU/USD: +1.00%

On the Radar

Date | |

|---|---|

Monday 01/06 |

|

Tuesday 02/06 |

|

Wednesday 03/06 |

|

Thursday 04/06 |

|

Friday 05/06 |

|